In this investment letter we provide an update on what is happening within the U.S. oil patch and its implications. When scanning news stories recently, we were surprised by the headline “Refracking is the new Fracking”.

We wondered, “What is refracking?” The question seemed rhetorical but worth exploring. The energy sector in the U.S. has been a leader in producing what is described as either disruptive technology or new and better ways of doing things, depending on one’s point of view. Refracking seems to be a clear example of that.

U.S. Oil Patch Update

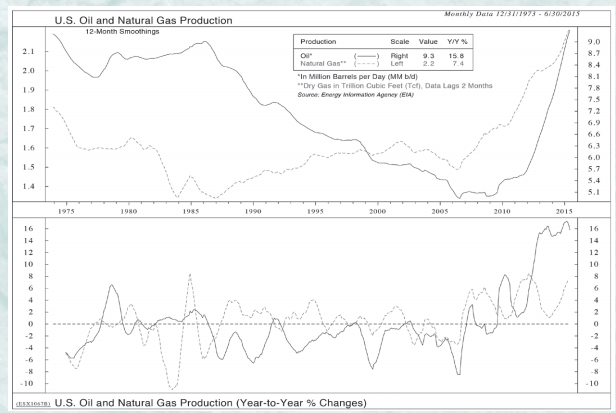

The top chart at left highlights the daily production of crude oil in the U.S. from the mid-70s and beyond 2012. After the trough in 2008-2009, production has steadily climbed to over 9 million barrels per day. With the U.S. crude oil benchmark WTI (West Texas Intermediate, a crude oil) trading at $40 per barrel at this writing, well operators need a cost-effective and productive method to boost production. Furthermore, as the Bloomberg article points out, America’s oil production is set to peak in 2020, less than five short years from now. Enter refracking.

Refracking: The Gift That Keeps on Giving

The refracking process is simple: Use water and sand to re-apply the procedure of blasting horizontal wells that were drilled during the shale boom in the U.S. Results have shown that oil recovery rises 60 percent or more and that wells can be hit repeatedly. Under the category of “you can’t make this stuff up” we learn that a well that has been refracked five times is called a “Cinco de Fraco”; a well hit eight times is an “Octofrac.”

As always, new techniques carry risks including inadvertently siphoning oil from adjacent wells and/ or ruining an entire reservoir. Yet when done right, refracking not only increases a well’s current output but also can raise reserves. But how cost-effective is the process? On average, drilling a new well costs $8 million while re-stimulating an old well costs $2 million. This belies the claim of marginal shale producers that they need a WTI benchmark of around $60 per barrel or higher to be profitable.

Economic Implications: The Trade Deficit

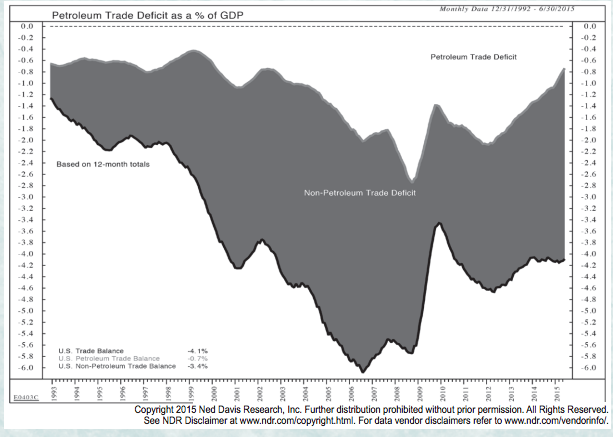

In our view, one of the biggest impacts of fracking vs. refracking is in the area of the trade deficit. The U.S. has for many years run a deficit, importing more than it exports. The chart from Ned Davis Research (below), covering the period from 1993 to 2015, depicts the trade deficit and the role of oil imports since 1993. Since 2008 the petroleum trade deficit has been declining steadily in line with steady increases in U.S. shale production. There are two ways to reduce a trade deficit: import less or export more. Because the U.S. dollar continues to appreciate, the likelihood of the U.S. importing less is low as foreign goods and services become cheaper. However, if regulators lift the barriers that limit our ability to send U.S. oil abroad, not only could the petroleum deficit be eliminated; our total trade deficit could be unwound. There are many knowledgeable and reasonable buyers of energy in Europe and other continents that would prefer to buy their energy from a more geopolitically stable provider like the U.S.

Conclusion

U.S. energy production continues to amaze as low crude oil prices have borne more cost-effective ways of increasing output. U.S. reliance on foreign oil can be reduced and the prospects for buyers of U.S. oil are waiting for regulations to line up with demand. Although stocks had been flirting with all-time highs, the risk of a correction in stock prices remains. We maintain a favorable outlook on stocks longer-term versus other asset classes like bonds and cash. We remain buyers of stock on weakness.