With a bumpy start to the year in stocks and a nice rally off the February 11 bottom, we are in and around the highs for the year in stocks. As the summer months approach, and with the seasonally weak periods in stocks, we turn our attention to what we call “The Big Three”: the Dollar, Oil and the Fed.

With a bumpy start to the year in stocks and a nice rally off the February 11 bottom, we are in and around the highs for the year in stocks. As the summer months approach, and with the seasonally weak periods in stocks, we turn our attention to what we call “The Big Three”: the Dollar, Oil and the Fed.

As we have mentioned in the past on these pages, the U.S. Dollar remains and will remain the world’s major reserve currency for the foreseeable future for a number of reasons. As a quick refresher, they are as follows: the vast majority of global trade happens in USD, approximately 64 percent of official foreign exchange reserves are in the currency, commodities such as oil and gold trade in USD and there is a military to back it up. Since oil among other commodities trades in U.S. dollars, we in the investment department need to be tuned in to the relationship between oil and the dollar AND the relationship between the dollar and the entity that controls the supply and demand for the currency, the Fed.

It is important to note that relationships between financial markets can and do change over time. A good way to measure the relationship between two things like different markets is correlation, which explains the strength of a connection or association. Correlation, according to the all-knowing Wikipedia, is defined as “any of a broad class of statistical relationships involving dependence, though in common usage it most often refers to the extent to which two variables have a linear relationship with each other. Familiar examples of dependent phenomena include the correlation between the physical statures of parents and their offspring, and the correlation between the demand for a product and its price.” However, correlation is not to be confused with causation. Just because there is a strong relationship between two variables does not mean that one causes the other to happen.

As an example: Suppose I sneeze and it rains in Africa. These two variables may have a high degree of connection but it would be absurd to think my sneezing caused rain in Africa. Let’s now examine the relationships between the USD, oil and the Fed.

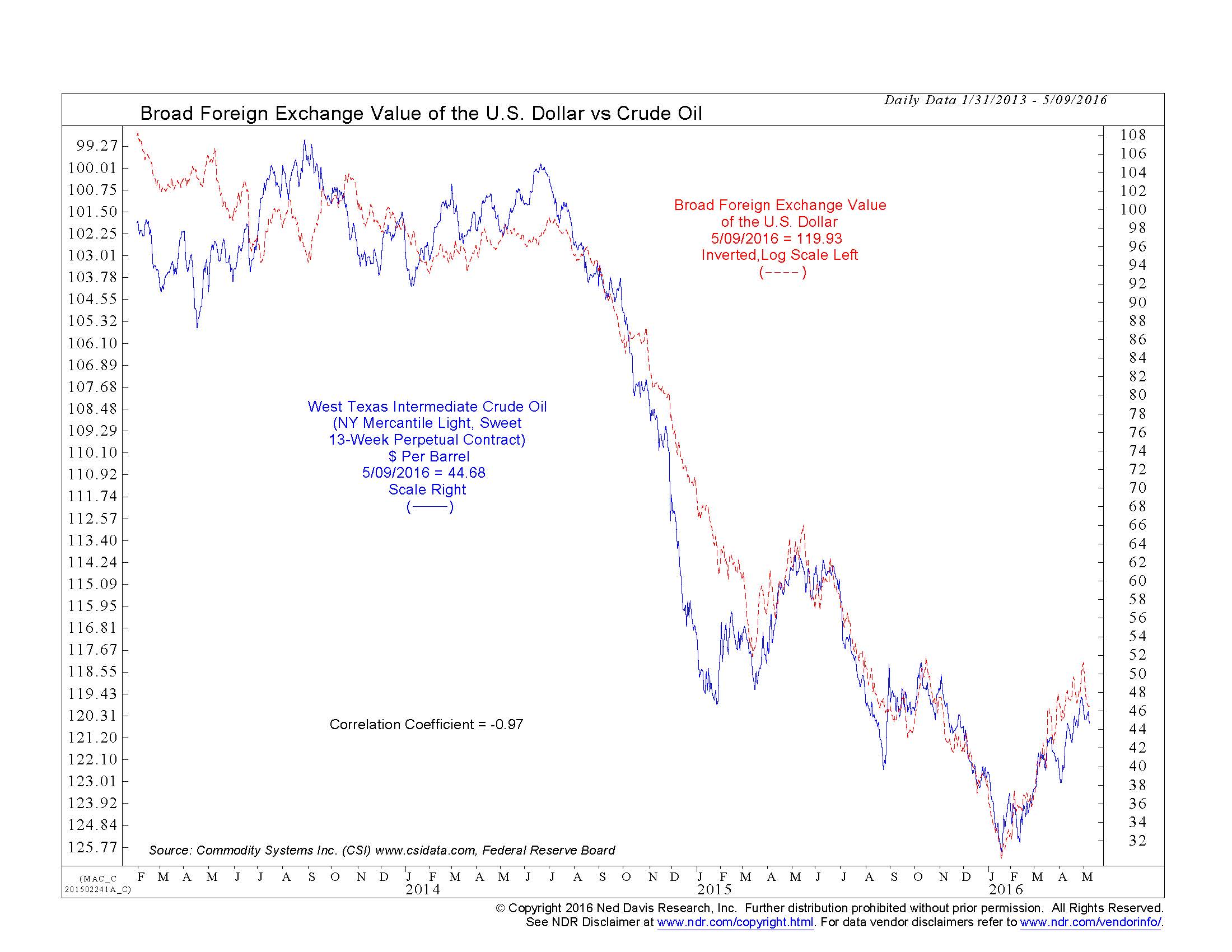

Between June 2014 and January 2015 oil fell about 55 percent using the NYMEX futures to track West Texas Intermediate (WTI). According to a February 2015 article by Joe Kalish, Chief Global Macro Strategist for the Ned Davis Research Group, the correlation between the USD and WTI crude was very strongly negative at -0.91. (For the math majors out there, that’s close to a perfectly inverse relationship between oil and the USD, as correlation is scored between +1, perfectly positive, and -1, perfectly negative). So as Kalish put it, “not only was surging shale production, a continued recovery in Gulf of Mexico drilling, a rebound in Libyan exports, further gains in Iraqi output, and the refusal of Saudi Arabia and other OPEC and non-OPEC nations to reduce production.

This supply glut, along with a reduction in demand due to slower global economic growth, sent prices plunging…. But the shale story was well known and sluggish global growth was nothing new. A 55.5 percent decline seemed excessive. There had to be another explanation. There is – the (rally in the) U.S. dollar!” In a recent update to that, a publication written in May 2016 noted that the inverse relationship has strengthened to -0.97, as seen in the chart on page 1.

If the USD is affecting commodities, particularly oil, what is affecting the USD? It is monetary policy, which is at the beck and call of—you guessed it: the Fed. With a June rate hike likely off the table, the oil market has the potential for a continued rally. Provided the markets and economic data hold up, we believe Q3 would be more likely for a resumption of rate normalization. That could push USD higher and stop the oil rally.

With a bumpy beginning to stocks in 2016, we continue to be of the mind that after getting a peak-to-trough correction in stocks of about 15 percent, the market has set the stage for resumption in the bull market that began in March of 2009. There have been and will be periodic corrections in bull markets and this one is likely the pause that refreshed. Besides supply- and-demand imbalances, there is a strong inverse relationship between the dollar and commodities, including oil—AND there is a strong direct relationship between monetary policy and the dollar. With the Fed at the controls on monetary policy, we see the next hike in Q3 and that’s it for rate increases in 2016.

About Caldwell Trust Company

Caldwell Trust Company is an independent trust company with offices in Venice and Sarasota, Florida. Established in 1993, the firm currently manages over $800 million in assets for clients throughout the United States. The company offers a full range of fiduciary services to individuals, including services as trustee, custodian, investment adviser, financial manager and personal representative. Additionally, Caldwell manages 401(k) and 403(b) qualified retirement plans for employers.