Half way through the year the domestic capital markets continue to consolidate as they have since the late January equity market sell-off and spike in Treasury yields. The fundamental underpinnings of the markets remain solid and increasingly the news flow out of Washington is dominating short term market action. With the exception of the technology driven NASDAQ domestic equity market returns are relatively flat with the S&P 500 index returning 1.67% and the Dow Jones Industrial Average down 1.81% at mid-year. The NASDAQ is up 8.79% for the year. Of note is the pick up in equity market volatility which has moved towards historically normal levels from the ultra-low levels of last year.

Half way through the year the domestic capital markets continue to consolidate as they have since the late January equity market sell-off and spike in Treasury yields. The fundamental underpinnings of the markets remain solid and increasingly the news flow out of Washington is dominating short term market action. With the exception of the technology driven NASDAQ domestic equity market returns are relatively flat with the S&P 500 index returning 1.67% and the Dow Jones Industrial Average down 1.81% at mid-year. The NASDAQ is up 8.79% for the year. Of note is the pick up in equity market volatility which has moved towards historically normal levels from the ultra-low levels of last year.Both mid-cap and small cap companies have turned in positive returns advancing 3.49% and 7.66% respectively year-to-date. The strong performance of small cap issues is directly attributable to the impact of tax reform and the perception of relatively negligible impact from potential tariffs and trade wars.

We continue to be in an environment where growth stocks outperform value stocks and the return differential in many cases is pronounced. For example, for large cap domestic stocks the differential depending on the indices utilized is 800 – 1000 basis points. While not as great the performance gap for domestic mid and small cap stocks is also meaningful. Given year-to-date market performance has been driven largely by growth-oriented stocks in the Technology and Consumer Discretionary sectors, clients with portfolios structured towards dividend paying defensive stocks (i.e. value stocks) have suffered from poor performance relative to the market in their investment portfolios. We believe this trend will continue for now, but we are cognizant of the narrow market leadership and potential impact of a sell-off in Technology shares.

Late in June Technology stocks sold off and consequently Consumer Discretionary shares have been the best performing issues thru mid-year. Both sectors are up over 10% for the year. Only the Energy and Health Care sectors have also turned in positive performances. Energy issues advanced just over 5% year-to-date and put in the best showing for the quarter posting gains north of 12%. Crude oil prices are currently back over $70 per barrel. The balance S&P 500 sectors have turned in negative results for the year. The Consumer Staple and Utility sectors have turned in the worst performance year to date with respective declines of around 10%.

All major Global and Regional equity indices are negative at mid-year. Developed International markets (as measured by the EAFE index) are down 3.27%; Emerging Markets are down 5.61%. The recent strengthening of the dollar has contributed to the poor returns.

Returns in the domestic and international fixed income markets are also largely negative year to date. The broad domestic bond market is down 1.62% at mid-year. That said both High Yield and returns on cash like fixed income products are slightly positive year-to-date.

The yield on the 10-year Treasury bond closed mid-year at 2.86%. The yield has retreated of late as talk of tariffs and trade wars has intensified. Earlier in the year the yield rose on inflation expectations and a pick-up in expected economic growth. The 10-year yield started this year at 2.40% rose to 3%+ earlier in this year and has subsequently declined.

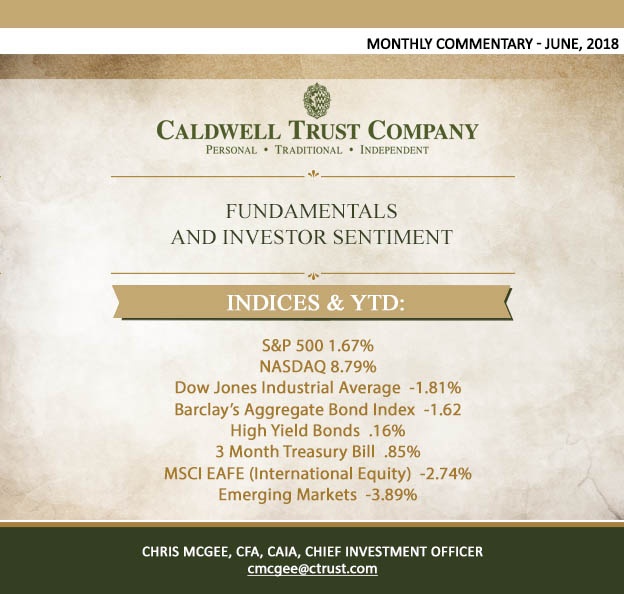

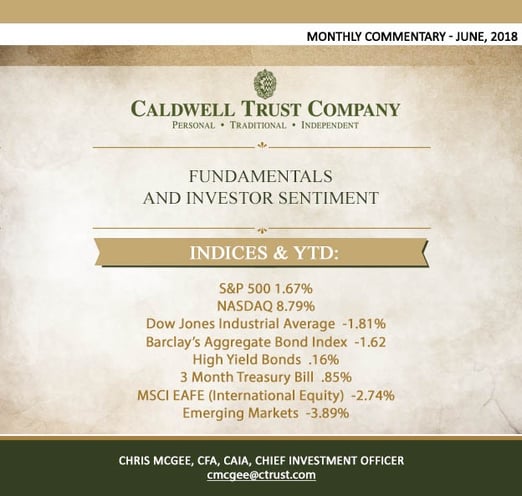

Major market index returns year-to-date thru June were as follows:

S&P 500 1.67%

NASDAQ 8.79%

Dow Jones Industrial Average -1.81%

Barclay’s Aggregate Bond Index -1.62

High Yield Bonds .16%

3 Month Treasury Bill .85%

MSCI EAFE (International Equity) -2.74%

Emerging Markets -3.89%