- Strong earnings for the Q1

- Headlines continue to dominate capital markets

- 10-year Treasury yield closes above 3%

- Energy stocks rally

Earnings season (Q1) is winding down with over 90% of S&P 500 companies having reported. Earnings growth on a year-over-year basis has exceeded 20% which is shaping up to be the best quarterly showing since 2010. Upside surprises on consensus earnings is tracking to be the best in 10 years. With the market correction earlier in the year and earnings revisions the forward price/earnings ratio on the S&P 500 is around 16X earnings. To a large extent high expectations by investors has resulted in companies being less rewarded for upside earnings surprises but punished meaningfully for earnings misses. The solid fundamentals underpinning equities continues to take a back seat to the latest headlines.

The 10-year Treasury yield closed above 3% for the week increasing more than 60 basis points since the beginning of the year. It will be interesting to see if the yield holds above 3% going forward. Even with the move higher rates remain at relatively low levels.

Domestic equity markets closed slightly lower for the week. Both the Dow Jones Industrial Average and the S&P 500 are essentially flat year-to-date; the NASDAQ has returned in the mid- single digits. Several retailers reported decent Q1 earnings results last week; energy was once again the best performing sector in the S&P. Crude oil closed above $70 per barrel last week and is at the highest level in four years. The more defensive S&P sectors continue to underperform on a relative basis.

The economic calendar includes the release of new home sales on Wednesday, and existing home sales Thursday. On Friday the Census Bureau reports preliminary durable goods orders for April.

Earnings is dominated by retailers once again:

Tuesday – AutoZone, Kohl’s, TJX, and Toll Brothers

Wednesday – L Brands, Lowes, and Target

Thursday – Autodesk and Gap

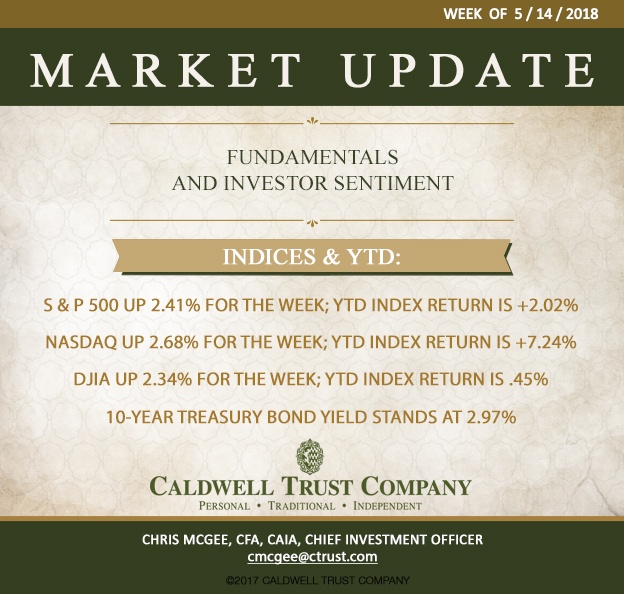

Indices for the week and YTD are as follows:

S & P 500 down .54% for the week; YTD index return is 1.47%

NASDAQ Composite down .66% for the week; YTD index return is 6.53%

Dow Jones Industrial Average down .47 % for the week; YTD index return is -.02%

Benchmark 10-year Treasury bond yield stands at 3.06% - up 6 basis points for the week.