-

Market fundamentals remain solid

-

Inflation expectations subside

-

The Fed meets shortly

- Equity markets rally on strong jobs report

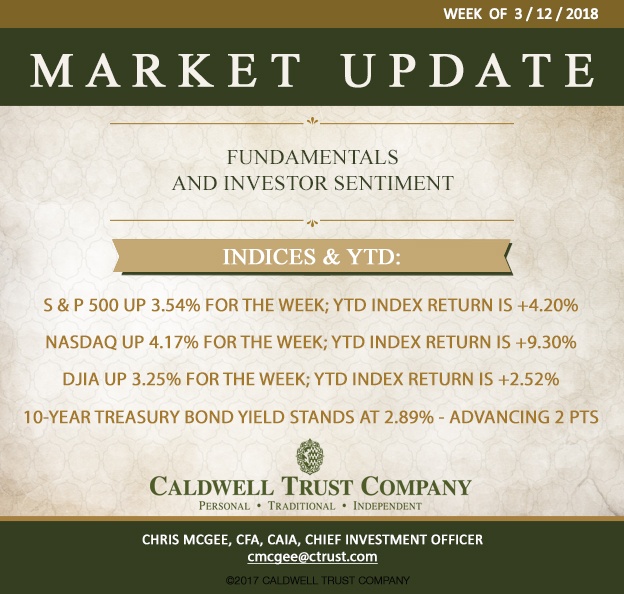

The week ended on a high note with the February jobs report showing robust job gains but not the wage gains shown in the January report. The broad domestic equity markets rallied on the news and the NASDAQ now shows gains year-to-date close to double digits. Both the Dow and the S&P 500 have registered low to mid-single digit gains for the year.

The yield on the 10-year Treasury bond has stabilized temporarily around 2.90%. The Federal Reserve Open Market Committee meets shortly and is anticipated to hike the Fed Funds rate; the consensus is that three rate hikes are in store for 2018.

Other positive news for the week included the prospect of President Trump meeting with North Korea and the saber rattling around tariffs and protectionism receding for the time being. All in all, the investment news flow was positive on the week.

As noted previously Q4 earnings season is virtually complete and results were strong. While the current economic expansion is long in tooth, given its subdued nature and the current market fundamentals we remain optimistic on the equity markets. At best fixed income markets domestically will be challenging.

The economic calendar for next week includes the Consumer Price Index being released on Tuesday. Retail Sales and the Producer Price Index is reported on Thursday.

Earnings reports for next week are sparse and Retail centric:

Tuesday – Dick’s Sporting Goods, DSW, and Williams Sonoma

Thursday – Adobe Systems, Dollar General, and Ulta Beauty

Indices for the week and YTD are as follows:

S & P 500 up 3.54% for the week; YTD index return is +4.20%

NASDAQ Composite up 4.17% for the week; YTD index return is +9.30%

Dow Jones Industrial Average up 3.25% for the week; YTD index return is +2.52%

Benchmark 10-year Treasury bond yield stands at 2.89% - up 2 basis points for the week.