- Major equity indices mixed once again

- Rotation toward value stocks continues

- Global capital markets performance excellent year-to-date

- Domestic bond yeilds remain range bound

As was the case last week both the Dow and the S&P 500 rose this week while the NASDAQ Composite slipped. Returns for the week were muted. It does appear the rotation we have been experiencing continues. An excellent article appeared in the WSJ Friday looking at the rotation in detail. As outlined here last week there has been a rotation out of the Technology sector into the Telecommunication and Financial sectors. The WSJ article (Growth Still Beats Value in Stock Fight by James Mackintosh– page B1) goes into further detail on the rotation. In fact, what is happening across every S&P 500 sector is movement from growth to value stocks. The article argues that part of the rotation is a consequence of the gains growth stocks have realized versus value stocks this year and really since the sub prime crisis. To provide perspective, this year alone, growth stocks have outperformed value stocks across the board (meaning in the large, mid, and small capitalization spaces) on average by better than a 2:1 margin. The larger question posed by the article is whether this is simply a result of growth stocks being overbought and expensive or does it signal a more permanent rotation based on the expectations that economic growth and inflation will pick up meaningfully? Time will tell but clearly the long slow grind higher of the domestic equity markets and growth stocks is a function of the low domestic economic growth and lack of inflation for several years now.

As good as equity performance has been domestically this year, it is important to note how uniformly well performance has been globally. A quick glance at the Global/Regional Indices published by Ned Davis Research indicate no losses in global markets – all performance is positive. Even bonds have turned in positive returns, albeit mid - single digits.

The Fed meets this week and is expected to end the year with one last hike in the Federal Funds rate by .25%. As noted previously, the consensus is for 3 more rate increases in 2018. Recent economic releases in aggregate are trending positive.

Next week on the economic calendar: Producer Price Index for November reported Tuesday; Consumer Price Index for November is released on Wednesday; Retail sales for November are reported Thursday.

Next week earnings reports are sparse but a number of companies we own are hosting analyst calls to discuss their outlook for 2018, they include Cisco on Monday (actually a shareholders meeting); 3M and Principal Financial Group on Tuesday; Honeywell and Eli Lilly on Wednesday, and MetLife on Friday.

Earnings reports:

Tuesday – VeriFone Systems

Thursday – Adobe Systems, Costco Wholesale, and Jabil

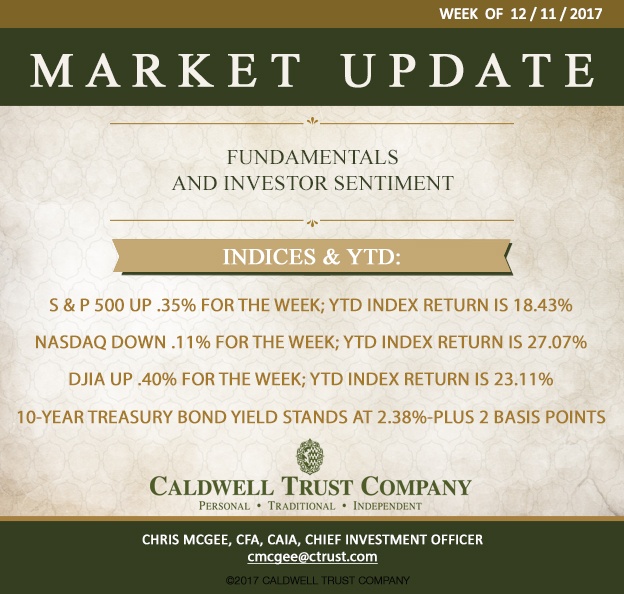

Indices for the week and YTD are as follows:

S & P 500 up .35% for the week; YTD index return is 18.43%

NASDAQ Composite down .11% for the week; YTD index return is 27.07%

Dow Jones Industrial Average up .40% for the week; YTD index return is 23.11%

Benchmark 10-year Treasury bond yield stands at 2.38% - virtually flat for the week (+2 basis points – again!)

----------------------------------------------------------------------------------------------------------------------------------------------------

Chris McGee heads Caldwell’s investment committee, which draws on a team of experienced in-house professionals and carefully chosen outside analysts to make decisions for client portfolios.

A Chartered Financial Analyst (CFA) and Chartered Alternative Investment Analyst (CAIA), McGee had previously been senior investment adviser and senior vice president at PNC Wealth Management in Sarasota for nearly a decade. Prior to that he was portfolio manager for five years with U.S. Trust (formerly Bank of America) in Sarasota. Before relocating here, he had served as vice president, capital management, for Wachovia Bank in Winston-Salem, North Carolina.