- Equity markets decline by 4%

- 10-year Treasury yield closes above 2.8%

- FOMC Leaves rates unchanged

- Q4 earnings growth continues to impress

- We remain bullish on equities long-term

The broad domestic equity markets sold off on above normal volume last week after 10 months of consecutive gains. Indices declines from their respective peaks on average are around 4%. A lot of the decline occurred Friday after the release of the latest jobs report which showed a pick up in hourly earnings in the January numbers. Many interpreted the report as further confirmation that inflation is picking up. The reality is that wage growth increased or contracted depending on your measurement period. Actual monthly hourly wage gains have remained relatively muted and consistent since the election.

More importantly, bond yields continue to rise as reflected in the 10-year Treasury yield closing the week at 2.84%. The yield has increased 40+ basis points (meaningfully) since the year commenced. Few pundits have the 10-year yielding above 3% by year end. As noted in previous blogs, the back up in yields reflects market expectations of a pickup in economic growth and inflation. While the current increase in yields has been fairly quick we remind readers that we are coming off of incredibly low levels from a historical perspective, and the increase in yields is a positive indication of economic strengthening.

In other interest rate news, the FOMC met last week (Yellen’s final meeting before Powell takes the helm) and elected to leave the Fed Funds rate alone. They did signal an increased inclination to raise short term rates if economic data continues to demonstrate strength. The consensus expectation continues to be three hikes in short-term rates this year. If you recall six weeks ago a lot of press was devoted to the negative implications of a flattening yield curve. Now we find that long rates are rising, and the curve is steepening with all its positive implications.

The sell off in domestic equities last week feels worse due to the absence of market volatility over the past year. In a piece published last August we looked at intra-year declines in the S&P 500 since 1980; on average the decline is 14%. To refresh everyone’s memory a market correction is a decline of at least 10%; a bear market is a decline of 20% or more. The markets are currently off their highs by 4%.

Given the positive and improving market fundamentals we remain bullish. The current market decline should be viewed as an opportunity to establish positions at a lower cost and to add to existing positions. Given the anticipation of rising rates we advocate adding to positions in the Financial sector and believe the more cyclical sectors like Industrials will continue to move higher. As evidenced by earnings last week Technology concerns continue to do well, and we would look to add to holdings on short term price weakness. The more defensive sectors (Telecommunications, Utilities, Consumer Staples, and Real Estate) that are yield oriented have struggled on a relative performance basis, and we believe will continue to do so as interest rates rise.

The economic calendar next week is relatively quiet. The Bank of England meets on interest rates. Several regional Fed presidents give speeches.

Next week is chock full of Q4 earnings reports yet again:

Monday – Bristol-Myers, Church & Dwight, Hess, National Oilwell Varco, and Sysco

Tuesday – Chipotle, Gilead, Disney, and GM

Wednesday – GlaxoSmithKline, Humana, Michael Kors, 21st Century Fox, and Yum China

Thursday – Twitter, Kellogg, Yum! Brands, and Tyson Foods

Friday – Moody’s and Pacific Gas & Electric

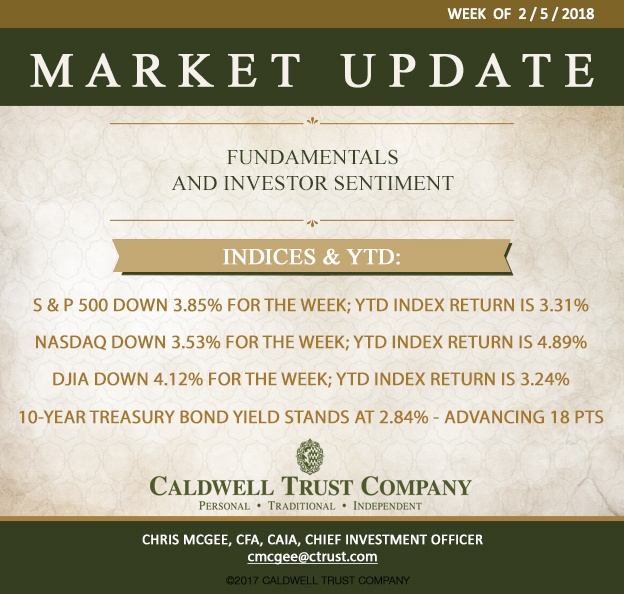

Indices for the week and YTD are as follows:

S & P 500 down 3.85% for the week; YTD index return is 3.31%

NASDAQ Composite down 3.53% for the week; YTD index return is 4.89%

Dow Jones Industrial Average down 4.12% for the week; YTD index return is 3.24%

Benchmark 10-year Treasury bond yield stands at 2.84% - advancing 18 basis points on the week